.svg)

“Digital transformation” is rapidly becoming a buzzword in financial crime risk management, both in the public and private sectors.

And with good reason.Technologies such as APIs and Privacy Enhancing Technologies (PETs) can drive multiple benefits, including automation, speed, flexibility, reliability, lower cost and secure data sharing.

But when is a digital solution truly transformative, rather than simply an enhancement of an existing process?

We explored this question in an in-depth discussion on technology organised by the German development agency, GIZ, together with representatives from regulatory bodies and the private sector. The session organisers encouraged participants to look to the future, imagining a “Dataland” in which technology has truly transformed approaches to dirty money.

Defining ‘digital transformation’

In an era when so many technologies promise wholesale innovation, how do we define true transformation? The Cambridge dictionary definition of transformation is “a complete change in the appearance or character of something or someone, especially so that that thing or person is improved”.

Clearly a “complete change” is a high bar, yet in the context of dirty money, a necessary one. Law enforcement, policy makers and academics agree that the financial system is remarkably ineffective in tackling financial crime.

The global standard-setter FATF, for example, has stated that “many countries continue to take a “tick box” approach to adopting laws and regulations, and don’t focus on results…countries need to make fundamental or major improvements to their money laundering and terrorist financing systems.”

In this context, it’s critical to remember that while technology can help to improve risk management systems, the core failings that facilitate financial crime are not just technical in nature. Rather, they’re related to incentives and decision-making.

Adopting financial crime risk management tech with the right incentives

When imposing penalties for money laundering failings, many jurisdictions publish documents outlining their background and legal basis. These documents can provide a unique insight into the inner workings of banks during periods in which the facilitation of illicit transactions was taking place.

In recent years, the largest penalties for facilitation of financial crime have resulted from a host of management mistakes and (in hindsight) poor decisions.Transaction monitoring systems did not fail; the alerts they generated were simply ignored. Compliance teams’ pleas for investment in better systems went unheard. And in some cases, financial crime was facilitated “knowingly and willfully”.

There is also little evidence that outcomes are improving over time. Penalties for failing to prevent financial crime have had at best a limited impact on financial performance and culture in the industry.

Technology is only as useful as its application, for instance if the alerts and intelligence generated by an automated system lead to decisions that meaningfully address financial crime risk.

A strategic approach to financial crime technology

That’s why at Elucidate we believe that the threshold for calling a technology or digital tool “transformative” is whether it can significantly change strategic decision-making regarding financial crime risk: Does any given solution provide both the intelligence and incentives to focus resources in areas where they can be of most use, for example?

Following this definition, our solutions include at least two examples of transformative technology applications. Drawing on in-depth knowledge of the financial industry and its approach to financial crime, these were specifically designed to shift incentives and strengthen decision-making at scale:

1. Financial crime risk ratings:

This is the assessment of banks’ financial crime risk using a benchmarked, quantitative metric - comparable to a credit risk rating.

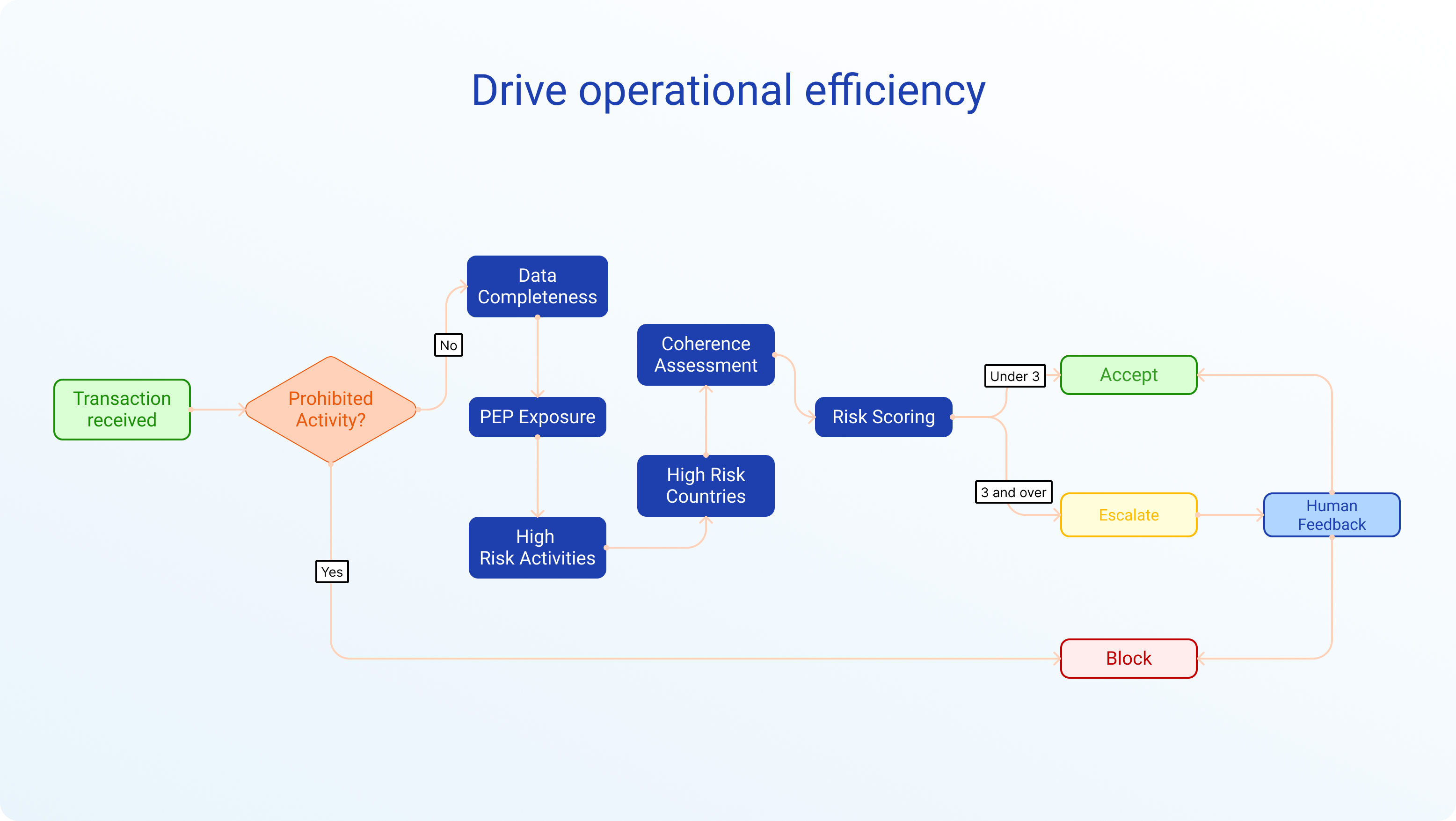

Elucidate’s risk ratings solutions are informed by our model which is an authorised benchmark by BaFin and is already being applied to over 340 banks on a monthly basis. It provides an overall risk score, scores for nine nuanced risk themes, and underlying findings based on quality assured data. From this, respondent banks can dynamically view their institution's risk profile against these nine themes, better target remediation programmes and provide tailored inputs for risk mitigation when working to maintain correspondent banking partners.

Our risk ratings solutions can also be used by correspondent banks to inform and track remediation programmes more effectively, ensure that their portfolio institutions use the same standardised system to manage their internal risks, thus saving cost and streamlining the risk management process.

This technology provides clear incentives for banks that must regularly share their risk scores with counterparties, since poorer scores motivate banks to strengthen their system; therefore providing a path to meaningful digital transformation.

2. Financial crime risk-based pricing:

At the moment, correspondent banks charge their respondents fees based on the volume of transactions, regardless of the risk exposure involved in each transaction. Market participants are therefore not incentivised to upgrade their financial crime controls for high-risk transactions.

By applying financial crime risk metrics to their networks, correspondent banks can adjust their pricing for individual respondent banks or groups of banks in their portfolio, creating immediate and measurable incentives for them to manage financial crime risk more effectively. You can read more about these incentives here.

The wide-ranging impact of strategic tech application and investment

From a public policy perspective a more strategic approach to financial crime risk technology can also serve to reduce wholesale loss of services and de-risking. Instead of naming a whole country as “high-risk” based on limited data, a technology-driven approach that reliably provides bank-level risk ratings, allows regulators and partner banks abroad to distinguish between banks in a particular country, and to assess their risk remediation progress over time and maintain relationships.

Therefore, by targeting the implementation of digital solutions to the root cause of financial crime, rather than operational distractions, institutions can improve friction in banking relationships, strengthen financial inclusion and meaningfully reduce financial crime.